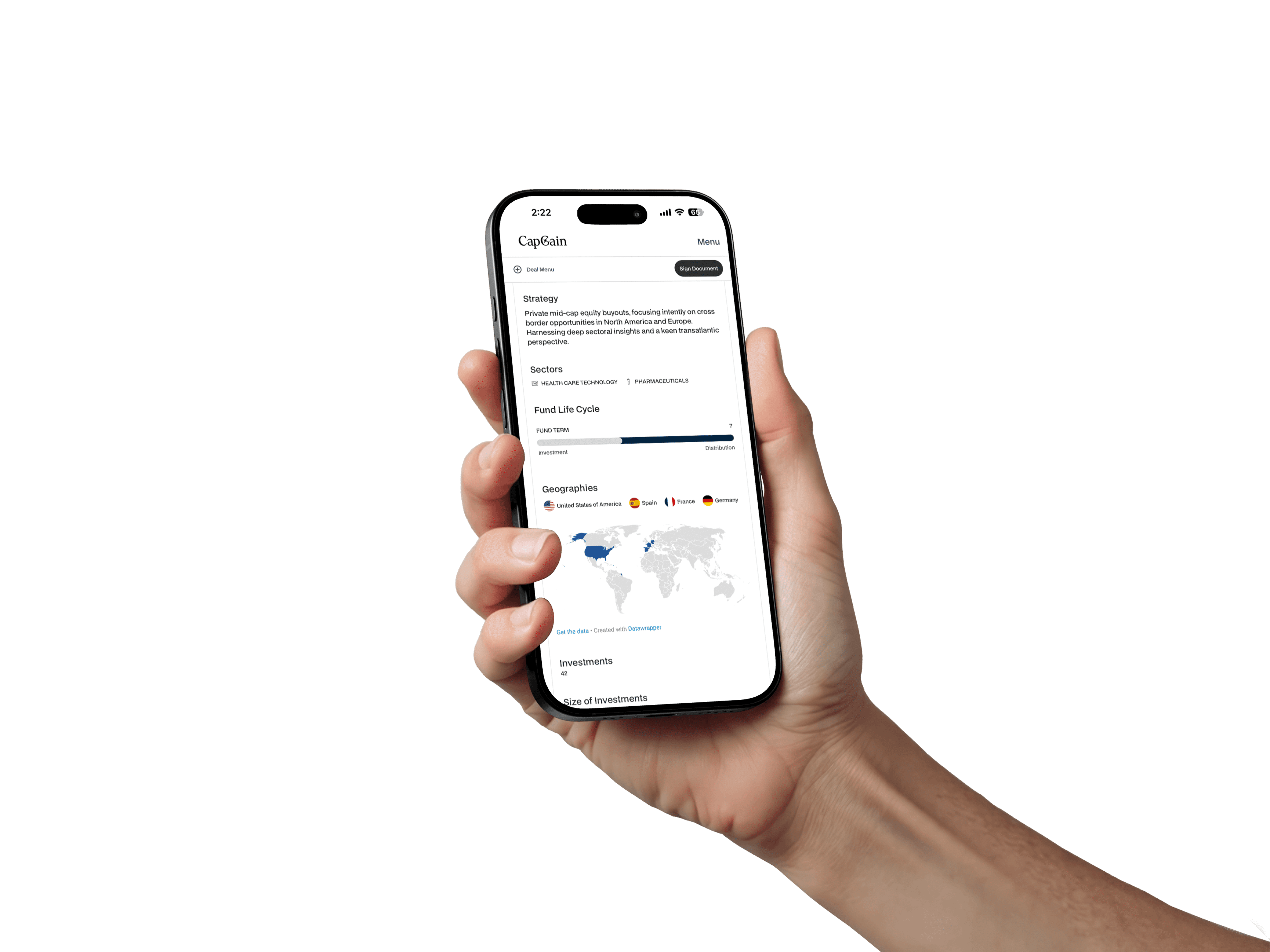

Private Credit

Private credit refers to loans made by non-bank institutions directly to companies, typically outside public markets. It’s part of the broader private markets ecosystem — sitting between equity and traditional bank lending.

How does private credit work?

Private credit funds raise capital from investors, then lend it to businesses that need flexible financing. Here’s how.

Private Credit

Private credit refers to loans made by non-bank institutions directly to companies, typically outside public markets. It’s part of the broader private markets ecosystem — sitting between equity and traditional bank lending.

How does private credit work?

Private credit funds raise capital from investors, then lend it to businesses that need flexible financing. Here’s how.

Private Credit

Private credit refers to loans made by non-bank institutions directly to companies, typically outside public markets. It’s part of the broader private markets ecosystem — sitting between equity and traditional bank lending.

How does private credit work?

Private credit funds raise capital from investors, then lend it to businesses that need flexible financing. Here’s how.

Formation

During the formation phase, the investment manager sets up the fund structure, defines its credit strategy, and begins engaging potential investors.

Phase 1

Fund Life cycle

Fundraising

providing credit

repayments

Marketing The investment manager promotes their upcoming fund to potential investors, outlining their investment strategy, risk and target return.

Here’s an overview of our upcoming investments.

Private Equity Fund Manager

The investors who are interested make capital commitments, according to their investment strategy and mandate.

Fund close

The manager now has the committed capital needed to start deploying into private credit opportunities.

Formation

During the formation phase, the investment manager sets up the fund structure, defines its credit strategy, and begins engaging potential investors.

Phase 1

Fund Life cycle

Fundraising

providing credit

repayments

Marketing The investment manager promotes their upcoming fund to potential investors, outlining their investment strategy, risk and target return.

Here’s an overview of our upcoming investments.

Private Equity Fund Manager

The investors who are interested make capital commitments, according to their investment strategy and mandate.

Fund close

The manager now has the committed capital needed to start deploying into private credit opportunities.

Formation

During the formation phase, the investment manager sets up the fund structure, defines its credit strategy, and begins engaging potential investors.

Phase 1

Fund Life cycle

Fundraising

providing credit

repayments

Marketing The investment manager promotes their upcoming fund to potential investors, outlining their investment strategy, risk and target return.

Here’s an overview of our upcoming investments.

Private Equity Fund Manager

The investors who are interested make capital commitments, according to their investment strategy and mandate.

Fund close

The manager now has the committed capital needed to start deploying into private credit opportunities.

Providing Credit

A specialised investment team reviews potential opportunities that fit the fund’s strategy. Each opportunity is screened against key criteria such as sector focus, financial performance, growth potential, and management quality.

Phase 2

Fund Life cycle

Formation

providing credit

repayments

Screening

The investment manager reviews a wide pipeline of potential borrowers, evaluating their credit quality, cash flows, and collateral. Only a fraction make it past this first screen.

Selection

Once a promising borrower is identified, the manager begins due diligence — analysing financials, business model, and risk profile — before negotiating loan terms.

Tailored loan solutions

Private credit funds provide bespoke financing, with terms negotiated directly between the fund and the borrower rather than set by standardised criteria.

When a borrower is approved for financing, the fund calls committed capital from its investors. Each investor contributes a portion of their pledged amount, ensuring the fund has sufficient liquidity to issue the loan. Capital distributions are allocated pro rata, based on each investor’s relative share of the fund’s total commitments.

Loan Issuance

Instead of taking equity, the fund extends a loan structured to align with the borrower’s capital needs, cash flow profile, and repayment capacity.

Assets under management

The difference between the total AUM and the capital deployed is uncalled capital - also known as dry powder. And the ratio between the two is ‘the capital overhang’.

Who are the borrowers?

Private credit caters to a diverse - and rapidly evolving - group of lenders

Providing Credit

A specialised investment team reviews potential opportunities that fit the fund’s strategy. Each opportunity is screened against key criteria such as sector focus, financial performance, growth potential, and management quality.

Phase 2

Fund Life cycle

Formation

providing credit

repayments

Screening

The investment manager reviews a wide pipeline of potential borrowers, evaluating their credit quality, cash flows, and collateral. Only a fraction make it past this first screen.

Selection

Once a promising borrower is identified, the manager begins due diligence — analysing financials, business model, and risk profile — before negotiating loan terms.

Tailored loan solutions

Private credit funds provide bespoke financing, with terms negotiated directly between the fund and the borrower rather than set by standardised criteria.

When a borrower is approved for financing, the fund calls committed capital from its investors. Each investor contributes a portion of their pledged amount, ensuring the fund has sufficient liquidity to issue the loan. Capital distributions are allocated pro rata, based on each investor’s relative share of the fund’s total commitments.

Loan Issuance

Instead of taking equity, the fund extends a loan structured to align with the borrower’s capital needs, cash flow profile, and repayment capacity.

Assets under management

The difference between the total AUM and the capital deployed is uncalled capital - also known as dry powder. And the ratio between the two is ‘the capital overhang’.

Who are the borrowers?

Private credit caters to a diverse - and rapidly evolving - group of lenders

Providing Credit

A specialised investment team reviews potential opportunities that fit the fund’s strategy. Each opportunity is screened against key criteria such as sector focus, financial performance, growth potential, and management quality.

Phase 2

Fund Life cycle

Formation

providing credit

repayments

Screening

The investment manager reviews a wide pipeline of potential borrowers, evaluating their credit quality, cash flows, and collateral. Only a fraction make it past this first screen.

Selection

Once a promising borrower is identified, the manager begins due diligence — analysing financials, business model, and risk profile — before negotiating loan terms.

Tailored loan solutions

Private credit funds provide bespoke financing, with terms negotiated directly between the fund and the borrower rather than set by standardised criteria.

When a borrower is approved for financing, the fund calls committed capital from its investors. Each investor contributes a portion of their pledged amount, ensuring the fund has sufficient liquidity to issue the loan. Capital distributions are allocated pro rata, based on each investor’s relative share of the fund’s total commitments.

Loan Issuance

Instead of taking equity, the fund extends a loan structured to align with the borrower’s capital needs, cash flow profile, and repayment capacity.

Assets under management

The difference between the total AUM and the capital deployed is uncalled capital - also known as dry powder. And the ratio between the two is ‘the capital overhang’.

Who are the borrowers?

Private credit caters to a diverse - and rapidly evolving - group of lenders

Repayments

As loans mature, repayments and interest begin to flow back to the fund. Active monitoring ensures borrowers meet obligations and preserves investor capital.

Phase 3

Fund Life cycle

Formation

providing credit

repayments

In the event that borrower’s circumstances change, loan terms can be adjusted to safeguard both borrower stability and investor capital.

Repayments

As loans mature, repayments and interest begin to flow back to the fund. Active monitoring ensures borrowers meet obligations and preserves investor capital.

Phase 3

Fund Life cycle

Formation

providing credit

repayments

In the event that borrower’s circumstances change, loan terms can be adjusted to safeguard both borrower stability and investor capital.

Repayments

As loans mature, repayments and interest begin to flow back to the fund. Active monitoring ensures borrowers meet obligations and preserves investor capital.

Phase 3

Fund Life cycle

Formation

providing credit

repayments

In the event that borrower’s circumstances change, loan terms can be adjusted to safeguard both borrower stability and investor capital.

Private credit in practice

Now that we understand how private credit works, let’s look at how it’s applied across real-world borrowers and strategies.

Why do borrowers choose private credit?

Private credit provides borrowers with faster, more flexible, and confidential financing solutions than traditional banks.

Speed & certainty

Faster execution than traditional banks, with less red tape.

Flexibility

Tailored structures—custom maturities, covenants, and repayment profiles.

Confidentiality

Private arrangements avoid public disclosures required in syndicated or public markets.

Non-dilutive capital

Founders retain ownership while accessing growth capital.

Private credit in practice

Now that we understand how private credit works, let’s look at how it’s applied across real-world borrowers and strategies.

Why do borrowers choose private credit?

Private credit provides borrowers with faster, more flexible, and confidential financing solutions than traditional banks.

Speed & certainty

Faster execution than traditional banks, with less red tape.

Flexibility

Tailored structures—custom maturities, covenants, and repayment profiles.

Confidentiality

Private arrangements avoid public disclosures required in syndicated or public markets.

Non-dilutive capital

Founders retain ownership while accessing growth capital.

Private credit in practice

Now that we understand how private credit works, let’s look at how it’s applied across real-world borrowers and strategies.

Why do borrowers choose private credit?

Private credit provides borrowers with faster, more flexible, and confidential financing solutions than traditional banks.

Speed & certainty

Faster execution than traditional banks, with less red tape.

Flexibility

Tailored structures—custom maturities, covenants, and repayment profiles.

Confidentiality

Private arrangements avoid public disclosures required in syndicated or public markets.

Non-dilutive capital

Founders retain ownership while accessing growth capital.

The private credit ladder: Mapping return and risk across strategies

From stable cash flows to complex opportunities: Private credit spans a broad borrower base — from mid-market businesses seeking growth finance to sponsor-backed firms and special-situation strategies.

Offering vs. origination

Understanding the difference between traditional bank loans and private credit

Banks offer loans as part of a relationship package - deposits, payments, and trade finance - relying on standardised checks around credit scores, collateral, and regulatory ratios.

Private credit funds originate loans through deep financial, operational, and downside analysis — structuring terms, covenants, and maturities to align borrower needs with investor return targets.

This shift transforms lending from a service to an asset class.

The private credit ladder: Mapping return and risk across strategies

From stable cash flows to complex opportunities: Private credit spans a broad borrower base — from mid-market businesses seeking growth finance to sponsor-backed firms and special-situation strategies.

Offering vs. origination

Understanding the difference between traditional bank loans and private credit

Banks offer loans as part of a relationship package - deposits, payments, and trade finance - relying on standardised checks around credit scores, collateral, and regulatory ratios.

Private credit funds originate loans through deep financial, operational, and downside analysis — structuring terms, covenants, and maturities to align borrower needs with investor return targets.

This shift transforms lending from a service to an asset class.

The private credit ladder: Mapping return and risk across strategies

From stable cash flows to complex opportunities: Private credit spans a broad borrower base — from mid-market businesses seeking growth finance to sponsor-backed firms and special-situation strategies.

Offering vs. origination

Understanding the difference between traditional bank loans and private credit

Banks offer loans as part of a relationship package - deposits, payments, and trade finance - relying on standardised checks around credit scores, collateral, and regulatory ratios.

Private credit funds originate loans through deep financial, operational, and downside analysis — structuring terms, covenants, and maturities to align borrower needs with investor return targets.

This shift transforms lending from a service to an asset class.

Investor benefits

Private credit offers access to stable, income-generating opportunities with enhanced yields, portfolio resilience, and structural protection through direct lending.

Higher yields

Direct lending captures an illiquidity premium, often delivering returns above public credit.

Diversification

Low correlation to stocks and bonds helps stabilise portfolios across market cycles.

Downside protection

Senior secured loans with bespoke covenants offer structural risk control.

Inflation hedge

Floating-rate structures adjust with interest rates, protecting real returns.

Stable income

Regular coupon payments provide steady, predictable cash flow.

We’ve built a platform

designed around you.

CapGain makes it easier for qualified investors to explore private market opportunities through a single digital gateway.

Access is restricted to Professional Clients as defined by the DFSA. Investments carry risk, and capital is not guaranteed.

Investor benefits

Private credit offers access to stable, income-generating opportunities with enhanced yields, portfolio resilience, and structural protection through direct lending.

Higher yields

Direct lending captures an illiquidity premium, often delivering returns above public credit.

Diversification

Low correlation to stocks and bonds helps stabilise portfolios across market cycles.

Downside protection

Senior secured loans with bespoke covenants offer structural risk control.

Inflation hedge

Floating-rate structures adjust with interest rates, protecting real returns.

Stable income

Regular coupon payments provide steady, predictable cash flow.

We’ve built a platform

designed around you.

CapGain makes it easier for qualified investors to explore private market opportunities through a single digital gateway.

Access is restricted to Professional Clients as defined by the DFSA. Investments carry risk, and capital is not guaranteed.

Investor benefits

Private credit offers access to stable, income-generating opportunities with enhanced yields, portfolio resilience, and structural protection through direct lending.

Higher yields

Direct lending captures an illiquidity premium, often delivering returns above public credit.

Diversification

Low correlation to stocks and bonds helps stabilise portfolios across market cycles.

Downside protection

Senior secured loans with bespoke covenants offer structural risk control.

Inflation hedge

Floating-rate structures adjust with interest rates, protecting real returns.

Stable income

Regular coupon payments provide steady, predictable cash flow.

We’ve built a platform

designed around you.

CapGain makes it easier for qualified investors to explore private market opportunities through a single digital gateway.

Access is restricted to Professional Clients as defined by the DFSA. Investments carry risk, and capital is not guaranteed.

Important Information

CapGain does not make investment recommendations and no communication, through this website or otherwise should be construed as a recommendation of any security. Alternative investments in private placements are highly illiquid, speculative, and involve a high degree of risk. Past performance is not indicative of future results. Investors may not get back their money originally invested and those who cannot afford to lose their entire investment should not invest. Prior to investing, carefully consider the respective fund documentation for details about potential risks, charges, and expenses. The value of an investment may go down as well as up. An investment in a private equity ("PE") fund or investment vehicle is not the same as a deposit with a banking institution. Investors receive illiquid and/or restricted membership interests that may be subject to holding period requirements and/or liquidity concerns. Investors who cannot hold an investment for the long term (at least 10 years) should not invest. In the most sensible investment strategy for PE investing, PE should only be part of your overall investment portfolio. The PE portion of your portfolio may include a balanced portfolio of different PE funds.

The CapGain platform may be accessed by certain international investors globally, including ‘Professional Investors’ (as defined by the DFSA) in the UAE, on a cross-border basis after appropriate checks and confirmation of their status. CapGain’s products are not suitable for retail investors in the UAE.